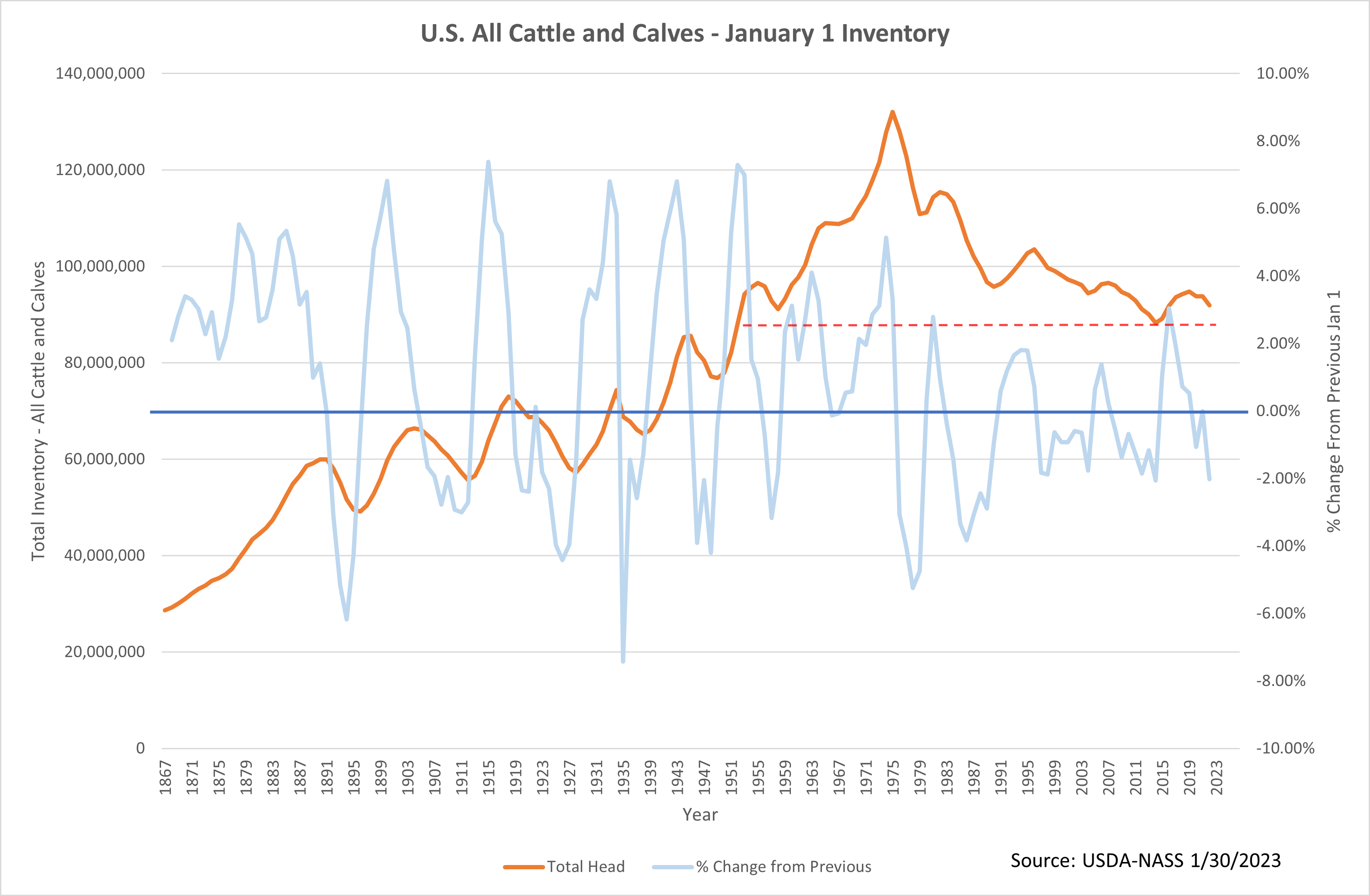

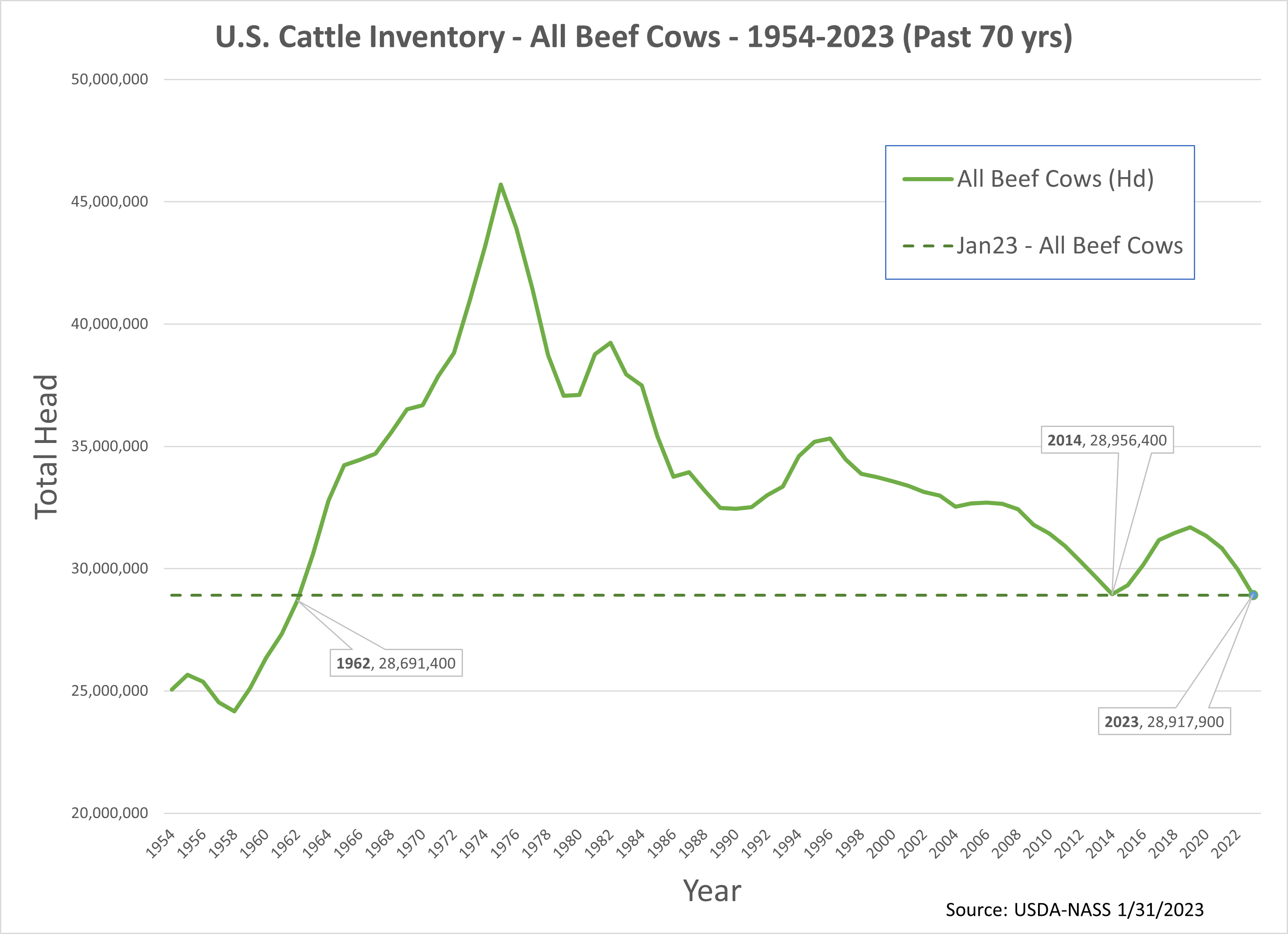

A couple of highlights of the USDA’s semi-annual survey report measuring U.S. cattle inventories as of January 1, 2023. The top-line category – “All Cattle and Calves” – declined by 3.04% relative to the (revised) 2022 inventory to 89.27 million head. This was a smaller decline than predicted by many industry experts. However, the last time this category declined by a greater percentage was 1987 (3.09%) The inventory of “Beef Cows” in the U.S. declined by 3.55% from the (revised) 2022 inventory level. The resulting 2023 Beef Cow inventory of 28.92m head is the lowest since 1962 (see chart). Links... View Article